UK Government says gigabit-capable coverage now sits at 81% of UK households

Cornish telco Wildanet has been awarded a £41m contract to roll out gigabit-capable broadband to more than 16,800 homes and businesses in East Cornwall, West Cornwall and the island of St Mary’s, located within the Isles of Scilly. The investment is part of the UK Government’s £5 billion Project Gigabit rollout to hard-to-reach homes and businesses.

It follows an investment of £36 million by the government in 2023 which saw Wildanet awarded two contracts to connect around19,250 homes and businesses in South West and Mid Cornwall. The announcement takes total Project Gigabit investment in Cornwall and the Isles of Scilly to £74 million, with the aim of connecting more than 37,000 premises

Initial work on network planning and surveys will start soon and installation works are expected to get under way in Autumn 2024.

Wildanet’s contract is one of half a dozen awarded today around the UK. The government said there is now 31 local and regional Project Gigabit contracts in place, representing more than £1.3 billion of investment to bring gigabit-capable broadband to over 780,000 hard-to-reach premises across the UK.

Gigabit progress

Since December, the government said it has signed 15 new contracts covering Kent, Leicestershire and Warwickshire, East and West Sussex, Bedfordshire, Northamptonshire and Milton Keynes, Buckinghamshire, Hertfordshire and East Berkshire, Nottinghamshire and West of Lincolnshire, West Yorkshire and York Area, East Gloucestershire, South Wiltshire, South Yorkshire, the Peak District, West Herefordshire and Forest of Dean, Cornwall and Isles of Scilly, Dorset and South Somerset, and Mid-West Shropshire.

Combined, these contracts represent more than £714 million of government investment to deliver gigabit-capable broadband to up to 370,000 premises. The government aims to award the first two call-off contracts under the cross-regional framework in the summer.

“We use the cross-regional intervention in areas where there has been minimal or no credible market interest in bidding for regional or local procurements, or where initial supplier appetite has fallen away,” it stated.

“We are engaging with the market for additional call-offs in areas including North Wales, South West Wales, North Somerset, South Devon, South and East Shropshire, North Herefordshire, Essex, and Central and North Scotland. We will also include the North East, as the awarded supplier for the previous procurement was unable to complete signature, as well as Mid Devon and South West Somerset, where supplier interest fell away during the previous procurement process,” it added. The supplier initially awarded the contract for Worcestershire is no longer able to sign so the government is currently exploring alternative options for this procurement.

Local telco

Wildanet, which has been backed by specialist alternative asset manager Gresham House’s sustainable infrastructure strategy with close to £100m invested since 2020, has grown to become a major regional employer, more than doubling its workforce in the last 18 months to over 220 staff as well as driving significant economic activity and employment through its commitment to using local businesses in its supply chain.

“The latest investment through Project Gigabit and the awarding of this contract is excellent news for Cornwall and for its many remote and hard-to-reach communities. It will help to bridge the digital divide, rectifying the historic imbalance in rural broadband provision whilst furthering the Government’s ambition to grow the economy by rolling out first-class digital infrastructure,” said Wildanet CEO Helen Wylde-Archibald (above left).

The plan is to give young people in the region skills in areas like AI, cybersecurity, digital marketing and entrepreneurship

Orange Digital Centers (ODC) are launching a free high-level certification training programme in partnership with Coursera, the online learning specialist.

The partnership aims to offer young people in Africa and the Middle East the opportunity to acquire skills needed in “digital professions”, free of charge and at their own pace via ODC’ 16 locations.

The skills are in areas such as AI, cybersecurity, digital marketing and entrepreneurship.

The 16 hubs are intended to further innovation and learning and are free and open to all, equipped with the latest technologies. They include a Code School, a Solidarity FabLab, an ‘Orange Fab’ and start-up accelerator.

There is also a fund, Orange Ventures Middle East and Africa, which invests in the most promising start-ups.

Asma Ennaifer, Executive Director CSR, Orange Digital Centers and Communication, Orange Africa and Middle East, says, “At Orange, we firmly believe that digital inclusion is the key to creating a fairer and more prosperous future for everyone.

“In partnership with Coursera and through the Orange Digital Centers, we are opening the doors of certification training to all our beneficiaries, offering educational and professional development opportunities to those who need them most.”

The move follows the Spanish government’s investment, widely seen as a counterbalance to Saudi Arabian telco stc’s stake in the company

CaixaBank’s main shareholder, Spanish holding vehicle Criteria, announced it had raised its stake in Telefónica to 5.007% from a previously reported 2.69%. CriteriaCaixa’s Chairman Isidro Fainé will seek to renew as a director of Telefónica at the telco’s next general shareholders’ meeting next Friday on behalf of CriteriaCaixa.

The investment follows the Spanish Government’s holding company SEPI announcing it had bought a 3.044% stake in Telefónica two weeks ago. The government’s holding is part of its plan to acquire a stake of up to 10% to counterbalance the acquisition of a large stake in Telefónica by Saudi Arabia’s stc.

According to Reuters, stc’s holding consists of 4.9% of Telefónica’s shares and financial instruments that give it another 5% in what it called “economic exposure” to the company. stc has still not requested government authorization to exercise the voting rights corresponding to the financial instruments.

Criteria did not say how much it paid, but a 5% stake in Telefónica has a current market value of slightly more than €1.14 billion. Last month CaixaBank reduced its stake in the telco to 2.51% from 3.51% previously.

In a media statement, CriteriaCaixa said the new stake was of a “strategic and long-term nature” and its investment objective was to provide the company with the “greatest shareholder stability” for “an essential company both for the country and for the industry at an international level.” In 2023, CriteriaCaixa received a total of €42 million dividends from Telefónica.

“La Caixa’s” relationship with Telefónica dates to 1987, when the then savings bank invested for the first time in the operator by acquiring 2.5% of its share capital. In 1996, it reached a 5% stake for the first time, which was diluted to 3.6% in 2000 after several capital increases undertaken by Telefónica to finance its international expansion.

In 2004, the stake recovered again above 5%. Although the investment was initially made by ”la Caixa”, in 2007 the stake became part of the perimeter of Criteria CaixaCorp, within the framework of the corporate reorganization prior to its listing on the stock market. In 2011, following the reconversion that led to CaixaBank’s listing, the bank began to hold the historic stake in Telefónica.

For its part, since 2017 CriteriaCaixa has built its own direct position in Telefónica’s share capital through purchases in the stock market. Following the transaction announced today, it now reaches 5.007%.

In all these years, both “la Caixa” first, then CaixaBank and now CriteriaCaixa, have maintained their presence in the governing bodies of the telco. Currently, that representation is held by Isidro Fainé, who is vice-chairman of Telefónica, and who has exceeded 30 years as a proprietary director this year.

Other major shareholders in Telefónica include BBVA and BlackRock.

Global Compute Infrastructure-owned firm raises PLN 1.35 billion to build in Warsaw and expand elsewhere in Poland

Polish data centre operator Atman concluded a PLN 1.35 billion agreement to finance the expansion of its data centre facilities. The loan is intended mainly for the construction of its new WAW-3 campus in Duchnice near Warsaw but will also be used for the expansion of Atman’s existing colocation facilities. The agreement was signed by 6 financial institutions from Poland and Europe.

Atman Data Centre Warsaw‑3 will eventually have 43MW of IT power. To begin operations there in Q4 2024, Atman will construct one (of three) colocation buildings and prepare custom-equipped data halls for the customers leasing entire data halls.

The WAW-3 DC campus will ultimately accommodate more than 50,000 servers in three buildings with a total area of nearly 19,000 sqm net for the collocation of IT equipment. The first stage of the investment started in October 2023, which was the construction of the first building offering 14.4MW of IT capacity, will be completed in the fourth quarter of 2024.

The move is a significant expansion for the company which currently claims a 15% share of the Polish data centre market in terms of net area for colocation, cloud computing and dedicated server services

Atman has operated in the market since 2011. In December 2020, the company was acquired by Global Compute Infrastructure, a global data centre infrastructure platform backed by the Goldman Sachs Merchant Banking Division and led by the former co-founders of Digital Realty.

Atman’s two existing data centre sites in Warsaw comprise eight colocation facilities of 10,500 sqm of IT space and 73MW of total power. The existing data centre campus is planned to expand by 3,600 sqm of colocation space in the future.

Largest loan

“The support provided to Atman by six leading financial institutions is the largest syndicated loan obtained in Poland for the development of data centres. The excellent condition of the company has been recognised by domestic and foreign financing institutions in the form of loans granted, which will enable further dynamic development of Atman as a leading data centre player in Poland and the CEE region,” said Atman CFO Wojciech Sadowski.

In addition to the standard financial requirements, the agreement places great emphasis on non-financial aspects related to energy efficiency and corporate sustainability (ESG) in all areas.

“We strongly believe in the success of our first European investment in data centres, which will give rise to further projects in this part of the world. We treat the construction of the WAW-3 campus as a flagship project of our capital group in the Central European region,” said Doug Lane, CFO of Global Compute Infrastructure, the main shareholder of Atman.

“According to many industry analysts, we are facing a great wave of growth in the data centre market,” said Atman CEO Sławomir Koszołko. “Atman is investing in the construction of new facilities, seeing good commercialisation prospects related to the growing demand for data centre services generated by the development of cloud computing and AI technology.”

He added: “In recent years, Poland has become a central data base in Central and Eastern Europe for the most important global entities in the IT industry.”

The Cassava Technologies business will use the energy for its Cape Town data centre (CPT1) first

Cassava Technologies owned Africa Data Centres and DPA Southern Africa (SA) – a joint company of the French utility, EDF – have broken ground on their solar farm in the Free State. The first phase will power getting its carrier-neutral CPT1 facility while the second phase will see power being supplied to JHB1 and JHB2 once wheeling agreements with relevant municipalities conclude.

This announcement is a key component of the 20-year Power Purchase Agreement (PPA) inked in March 2023 with DPA SA. Cassava Technologies president and group CEO Hardy Pemhiwa said: “This initiative positions Africa Data Centres as a trailblazer in the data centre industry in responding to South Africa’s energy crisis through sustainable technology solutions. This is in line with a broader industry shift towards innovative, eco-friendly practices.”

He added: “The strategic use of solar power showcases technology’s role in pioneering solutions for energy challenges and environmental sustainability.”

“[The] announcement represents a significant stride in our initiative to energise South African data centres sustainably, advancing our objective of achieving carbon neutrality,” said Africa Data Centres CEO Tesh Durvasula. “The first phase involves constructing the 12MW solar infrastructure to power our Cape Town data centre, with subsequent phases extending to our Johannesburg data centres.”

“Africa Data Centres, as a pioneer in the data centre industry, has consistently demonstrated a strong commitment to sustainability, aligning seamlessly with our company’s values. We are thrilled and honoured to contribute to Africa Data Centres’ mission of achieving carbon neutrality, beginning with the establishment of this solar power plant in the Free State to serve their data centre in Cape Town,” said DPA SA CEO Nawfal El Fadil.

“At the heart of our collaboration lies a shared understanding that the path to carbon neutrality extends beyond infrastructure—it demands innovation, expertise, and collective determination to overcome challenges. DPA SA, backed by EDF’s legacy, brings a wealth of experience and a proven track record in delivering high-quality, sustainable energy solutions to this partnership,” he added.

This project is a key element of Africa Data Centres’ plans to emerge as the “most sustainable colocation provider” on the continent. “Beyond procuring renewable energy, our commitment to an efficiency strategy has earned us the internationally recognised ISO50001 certification for the effective operation of our data centres,” said Durvasula.

“Data centres worldwide face scrutiny for their reliance on grid power and renewables, and Africa is no exception. Africa Data Centres is actively addressing this issue by generating renewable energy, alleviating strain on the local grid. Additionally, our sustainability objectives encompass achieving net-zero status at all facilities, making this project another significant stride towards reaching that goal,” he added.

Pictured left to right, all from Africa Data Centres: CEO Tesh Durvasula; business operations & strategy executive Wabo Majavu; CFO Finhai Munzara

Partner content: Network-native security services made it easier for consumers and SMEs to adopt them – and now mobile and fixed no longer have to be separate

Once, the security services that Communication Service Providers (CSPs) offered their consumer and small business customers consisted only of endpoint solutions, the apps that the customer needed to install and configure (and maintain and update) by themselves. This seemed like a good idea. However, consumers and small businesses, for the most part, do not have the tech savvy to implement their own solutions. This led to very low pickup rates for these apps/services. Then came network-native security services which run from the CSP’s network, thus removing the burden of operation from the customer.

But there was still a missing element. Customers who subscribed to the same CSP for both mobile and fixed connectivity still had one interface for their mobile security services and another for their fixed. Then came along converged security services.

What is converged security?

When we talk about converged security, we refer to the integration of cybersecurity services for both mobile and fixed broadband customers which are unified into a single orchestrated user experience. This can be true for consumer and small business customers alike. CSPs, often telecom operators doubling as ISPs, have long pursued convergence solutions, seeking to consolidate and streamline their offerings under one umbrella. The advent of converged customer security services presents CSPs with a myriad of business benefits compared to standalone alternatives, including cost reduction, enhanced customer experiences, and brand differentiation.

In a 2023 global CSP survey by Coleman Parkes Research, commissioned by Allot, although 94% of CSPs expressed interest in convergence, including security convergence, 3 in 4 said that they were held back because of their legacy systems. While this is a real concern, the validity of this barrier could be coming to an end. Among the new batch of customer-oriented security solutions, there are those which now orchestrate multiple systems across networks, even from other vendors. This opens the door for CSPs to a new opportunity that was not available before.

Converged security is network native

Converged security solutions go hand-in-hand with a network-native approach to customer security, leveraging services embedded within the CSP’s network infrastructure. While standalone mobile or fixed security services are viable options, their true value emerges when unified into a cohesive solution, catering seamlessly to both customer segments. However, CSPs face formidable challenges in implementing such solutions, grappling with traditional IT barriers and lengthy time-to-market delays for new offerings. Convergence fundamentally addresses these obstacles, paving the way for improved operational efficiency and customer satisfaction.

Together with a network-native security solution, a converged fixed and mobile security service delivers a unified security experience on all of the end-user’s devices. The user can be protected from cyber threats and have parental controls on all of those devices without installing a single piece of software, and without regular updates and maintenance. Adding the service is as easy as accepting an offer from the provider and all the customers’ devices are protected, whether connected to the mobile network or to the home router. The customer also gets better value for converged services which they might not have purchased if they were not converged, leading to increased revenue for the CSP even while the customer feels that they are getting a better deal.

One solution for all devices

Historically, CSPs have provided security solutions to consumer and small business segments, recognizing their appetite for CSP-delivered security services. Yet, the management of disparate security solutions poses significant hurdles, requiring separate monitoring, maintenance, and support infrastructures for each service type. This fragmentation not only increases resource expenditure but also stifles revenue potential, with standalone endpoint solutions often plagued by low adoption rates due to their complexity. Converged security solutions, which are inherently network-native, alleviate these pain points, promising a hassle-free security experience and enhanced protection for end-user devices and data.

The convergence of fixed and wireless infrastructure, propelled by advancements like software-defined networks, fosters a more harmonized telecom ecosystem. This convergence not only streamlines service delivery but also augments the efficacy of security measures by pooling threat databases across networks. Global surveys underscore CSPs’ keen interest in converged security solutions, driven by a quest for comprehensive threat detection, compatibility, scalability, and superior customer experiences. The integration of identity management, threat detection, and centralized monitoring forms the bedrock of converged security, promising consistent and robust protection across diverse services and platforms.

Benefits of converged security

In addition to bolstering operational efficiency and customer satisfaction, converged security solutions yield tangible financial benefits, including heightened ARPA and improved customer retention rates. By consolidating management processes, provisioning, and support services, convergence enables CSPs to streamline operations, reduce costs, and accelerate net-adds. Furthermore, convergence enhances CSPs’ competitive edge, positioning them as comprehensive service providers capable of meeting diverse customer needs across wireless, fixed, media, and IoT domains.

Converged security solutions enable transparent, unified provisioning, giving the end user the perception of a single provider and a single experience. Once provisioned, converged fixed and mobile security delivers a unified reporting experience which is activated on a regular basis to keep the end user updated regarding their security situation. This unified experience also offers the CSP opportunities to communicate with subscribers with branded messages. As a converged network-native solution, all the complexity of management and updating is hidden from the end user. On the CSP side, the implementation and configuration of the solution is also simplified by the fixed and mobile management umbrella tool.

Transcending better operations

Crucially, convergence transcends mere operational enhancements; it fosters a superior customer experience by offering streamlined account management, enhanced service offerings, and robust self-service capabilities. Moreover, by integrating security seamlessly within the network, CSPs can shield end-users from threats proactively, mitigating risks before they reach individual devices. This proactive approach not only enhances security but also instills confidence in customers, fostering long-term loyalty and brand advocacy.

Converged security solutions express the vision of the future of telecommunications, empowering CSPs to deliver unparalleled value and protection to their customers. By embracing network-native approaches and consolidating security services, CSPs can unlock a host of benefits, from cost savings and revenue growth to enhanced customer experiences and brand differentiation. As the telecom landscape continues to evolve, convergence, and specifically security convergence, emerges as a core strategy for CSPs seeking to thrive in an increasingly interconnected world.

Vikram Singh is Senior Director Cyber Marketing at Allot

About Allot

Allot Ltd. (NASDAQ: ALLT, TASE: ALLT) is a provider of leading innovative network intelligence and converged security solutions for service providers and enterprises worldwide, enhancing value to their customers. Our solutions are deployed globally for network and application analytics, traffic control and shaping, network-native security services, and more. Allot’s multi-service platforms are deployed by over 500 mobile, fixed and cloud service providers and over 1000 enterprises. Our industry-leading network-native security-as-a-service solution is already used by many millions of subscribers globally.

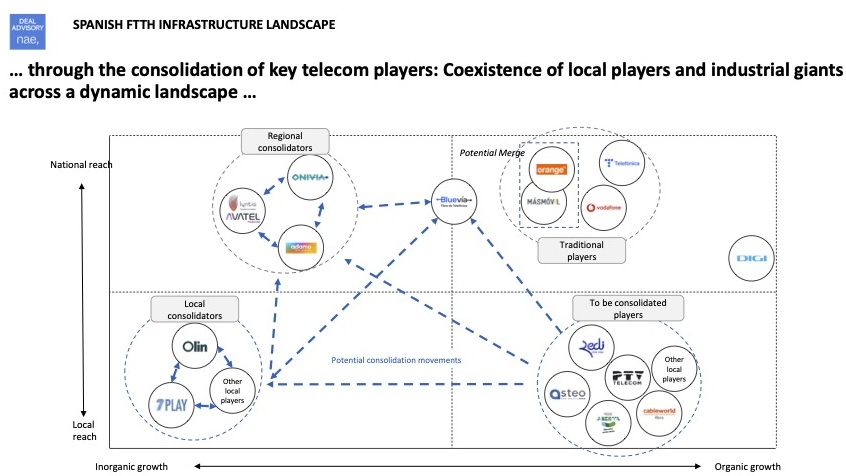

One of Europe’s leading FTTH markets is a test case for what happens when fibre networks overbuild

The acquisition of Digi Spain’s fibre-to-the-home (FTTH) network by Macquarie Capital and partners, abrdn and Arjun Infrastructure Partners, has brought the focus back onto just how overbuilt the Spanish market is with fibre and the inevitable consolidation path the market will follow.

Spanish and Latin America telecom consultancy Nae has been tracking the market closely and have come up with the term consolidation clock to help understand which operators may become the consolidators and which may be looking to exit the market.

Digi’s network will be run by Macquarie’s wholesale fibre company Onivia which, following the acquisition, will increase its coverage to around 10 million Spanish homes, more than a third of homes in the country.

Market leading deployments

Today eight out of every 10 broadband lines in Spain are fibre, a figure that exceeds the data for France, Italy, Germany or the United Kingdom. Spain moved early to establish the appropriate framework for operators to invest in fibre and now enjoys a very high level of coverage. The market is brimming with Tier-1 to alternative and rural FTTH operators it is is also the market that will see consolidation and new fibre models, particularly in the regions, first.

Nae recently carried out a consolidation analysis of the Spanish market and concluded, investors and operators are in for a bumpy ride. Spain is a sophisticated market although it has a major challenge with respect to overbuild due to low deployment costs.

According to Nae, due to this large number of homes passed deployed, Spain is materially overbuilt compared to other European countries by a factor of 3.1 times versus a market like the UK – which is already seeing altnets merge or fail – which is 2.6 times.

Nae director Joaquín Guerrero told Mobile Europe that the consultancy uses network overlap models to work out how good future merged partners may look. New deployments are, in fact focussed in low or no overlapped areas,” he said. “But there are huge exceptions. Digi choose to build a brand-new network directly overlapped with Telefónica and MásOrange. This network is being to be acquired by Onivia that already has building units (formerly from MásMóvil) overlapped with the Digi network.”

Complex wholesale market

The high overbuild ratio in Spain has led operators to open their networks, creating a highly complex wholesale ecosystem with a large number of operators and agreements between them. In the centre in incumbent Telefónica. Tier 2 ISPs run their own agreements, but Guerrero said the potential merger of two of them might bring significant changes to the ecosystem. Most of the major Tier 3 ISPs operate their own infrastructure, whilst simultaneously leveraging their operations on third-party networks to provide nationwide services.

“The overall FTTH ecosystem is already transforming: Telefónica´s BlueVia creation, the brand new MásOrange, the Onivia acquisition of 6 million homes passed from Digi, the sale process of Avatel or the Fi Vodafone contract renegotiation are some examples,” he said. “Not to mention the announced plans of Zegona to create a Netco with the former Vodafone HFC network. Almost every agent is changing their role in the ecosystem. And we think consolidation will be the norm in the future.”

He said high penetration and urban overbuild drive the exploration of opportunities for expanded growth in rural areas but this doesn’t come risk-free. “Rural deployments are harder and more expensive,” he said. “Creating a compelling business case for rural is also harder and you need to be both realistic and optimistic drawing your take-up curve.”

He added: “The bigger risk is, again, overbuild. If your assumptions include to be ‘the only FTTH network in a rural area’ for a long period, your business case will crash if a local overbuilder arrives.”

There are another kinds of deployments right now, he added, around densification. “Trying to connect small pools of homes in urban or semi urban areas left unconnected by the first deployments (municipalities licences, landlords, hard geotype and so on,” he said.

Nae’s research has mapped out the distribution of each operator’s infrastructure network, segmented by urban (3.3x overbuild), semi-urban (2.1x overbuild), semi-rural (1.7x overbuild) and rural footprints (1.2x overbuild). As a result, nuances in strategy emerge. “Telefónica has carved out its rural network in BlueVia but has the wider national coverage. The brand new MásOrange has also a very wide footprint combining the urban deployment of Orange and the more rural of MásMóvil,” he said. “Digi has specialised in very dense urban areas vs Adamo very focussed in rural areas.”

The market has ended up with urban giants, rural pioneers, and an abundance of small-regional operators like Avatel/Lyntia leading several municipalities. “The presence of “other” builders [outside the biggest FTTH providers] is very important – comprising rural (19%) and in semirural (23%),” he said. “And this “others” [category] is a full-scale ecosystem with, literally hundreds of players of very different sizes and strategies!”

He added: “We have identified at least 300 municipalities where the “incumbent” operator is a local one.” In urban areas he pointed out that Digi uniquely makes up the “others” in urban areas.

Consolidation time

Nae found that the main FTTH operators show high overlap levels while 60% of the challengers, due to their regional approaches have a low overlap level. “We are envisioning a multistep consolidation process, and these local operators will be included from the very beginning. This is the role of companies like Avatel, Excom or 7Play,” he said.

Using the figure above, Guerrero calls this process the consolidation clock. “In some way many of the small local players (in D quadrant) will migrate to C quadrant as they will be consolidated by local consolidators, and this will be integrated by regionals (A) who eventually will move to B or be acquired by major players,” he said.

“But this process is not going to be so smooth,” he added. “Maybe the prices to be paid does not fit with the current expectations of sellers? Or may be some networks are just left. How much time it will take is hard to say, but the announcement from Onivia and Digi is a symptom that things moving forward quickly.”

ServCo and InfraCo

These consolidation movements also lead us into new business models by splitting a traditional operator into infrastructure and services organisations – changing the current ecosystem. Under these new ecosystem rules, Nae believes an oligopoly scenario could appear where two or three InfraCo players own all the networks.

“In the Spanish market we have already three big “neutral” FTTH networks: Onivia, Elanta (Lyntia) and BlueVia,” he said. “All the local consolidators have also developed (or are developing) a wholesale offer. Nevertheless, the bigger part of the final fixed broadband market is owned by vertically integrated players (Telefónica and, now the leader, MásOrange) so we are very far from a perfectly “delayered” solution, and may be, we will never get there.”

“So, we foresee a consolidation process around the networks of the two vertically integrated operators (MásOrange and Telefónica),” he said. “Is there place for a third, more urban, network? This is the hardest question!”

The functional or even structural splits will cause other ructions. “Will Telefónica and MásOrange do some form of carveout in their networks? Very likely in a medium timeframe,” he said. “And for sure high interest rates are not good for telco infrastructure investments!”

Guerrero said regulating this type of markets is going to be a nightmare for European regulators. And this chapter is yet to be written. “All the major FTTH networks are already open and there [is] wholesale competence (Fi is currently renegotiating their contract with Vodafone for instance),” he said.

“The point here is the level of infra competence we need as industry or society. Is two [InfraCos] enough? How much is three is better? We need to find the answer,” he said. “Personally, I would find more ‘vibrant’ a scenario with three more specialised players, but we need to match this with a predictable, big enough, cash-flow generation machine.”

Onivia the consolidator

Commenting on the Digi transaction Onivia CEO Jose Antonio Vázquez Blanco said “With this acquisition, Onivia confirms its position as largest neutral and independent player, enhancing the value-added proposal for our telco customers, increasing coverage, and offering latest XGS-PON technology. It is also a fantastic step towards our national end-to-end telco proposal for other market segments such as utilities and alarms.”

The network acquired currently comprises approximately 4,250,000 homes passed with the rest of the network, covering up to 1,750,000 homes passed, to be deployed over an estimated period of three years. This would see the network reach a total of 6 million homes passed, covering 12 provinces across the regions of Madrid, Segovia, Avila, Castilla-La Mancha, Comunidad Valenciana and Murcia.

The transaction also provides the consortium with the option to acquire any future fibre rollouts from Digi in those provinces, subject to certain conditions. Digi will continue to use the FTTH network to serve its own customers and remain as anchor client, with the network made available to all other Onivia customers.

Minister also asks hyperscalers to help Africans implement AI across the continent

The South African Government announced it wants to connect 5.5 million households in rural areas and townships to the internet via wi-fi hotspots over the next three to four years, according to Minister of Communications and Digital Technologies Mondli Gungubele speaking to press last week.

Despite some progress in the country, in 2023, only 10% of South African households had access to the internet at home according to the Independent Communications Authority of South Africa (ICASA).

“We are committed to bridging the digital divide by providing wi-fi access to communities and ensuring universal access to the internet,” he said, adding that the government service costs ZAR 5 ($0.27) per day for one gigabyte and from 250 rand per month for an unlimited plan.

The government initiative is part of the second phase of SA Connect, launched in November 2023, of the nation’s broadband policy originally launched in 2013. When complete, it aims to provide 80% of public administrations, communities and homes broadband access in three years, according to Ecofin. Phase 1 of the project focused on providing 10Mbps Internet connectivity to nearly 970 essential public administrations.

AI support

Minister Gungubele also told attendees of the National AI Government Summit last week that public policy making, and frameworks must adapt to address the governance imperatives of AI and emerging technologies to protect globally agreed human rights.

“There are areas that are traditionally the exclusive mandate for governments to conduct its business. Areas such as defence, safety and security, social security net- support and intelligence gathering, amongst others come to mind. These are areas where government must lead in the adoption of AI,” said Gungubele.

“There are, however, other areas where the direct role of government is expected through policy formulation and regulatory approaches that will safeguard the preservation of livelihoods and creation of sustainable jobs. In this area, the adoption of AI must ensure the ethical and impactful purposive delivery, he added.

The minister noted several AI initiatives on ther continent like AI in Africa Machine Learning Indaba, conducted by South Africa; the release of the Africa AI Blueprint by Smart Africa Alliance; and South African government’s endeavour to establish the Artificial Intelligence Institute (AIISA) and Centre of Artificial Intelligence Research (CAIR). The government wants to develop at least 11 AI hubs in AIISA ranging from ranging from built environment, just energy transition, health, media and languages.

He called on cloud companies “such as Microsoft, Google, Huawei, Nokia, and Amazon Web Services, amongst others”, to continue establishing AI research centres in Africa.

“For Africa to be competitive in the world, we need to realise that there was a space race, then the arms race and now the AI race. We cannot afford to be left behind in this one. The onus is upon us to participate in this AI race through a coordinated and collaborative approach,” he said.

“We require venture capital funds that are focused on and dedicated to Artificial Intelligence. Lastly, we need to realise collaboration between government and private sector in AI research,” he added.

The summit was convened for the government and the private sector to initiate a policy and regulatory framework to guide and “leverage the advances in AI for human good”.

Britain’s RAC Foundation said the country’s “patchy” mobile signal coverage is causing problems for EV drivers

Around two-thirds of the UK’s most common type of public chargepoints suffer limited mobile signal connectivity meaning they do not have an adequate level of coverage from all four mobile phone network providers – EE, O2, Three and Vodafone – to guarantee they can be activated 100% of the time.

The RAC Foundation found that outside of London, just a third (33.4%) of the so-called Type-2 chargers analysed are in locations where there is acceptable all-network 4G coverage. Two-thirds (66.4%) are in spots where a signal from one, two, three or even all the providers is absent or too weak to work. In London, the picture is only slightly better at 39.7% and 61.3% respectively.

According to Department for Transport figures (based on data from ZapMap) there were 53,677 public charging devices in the UK at the start of the year.

Of these, 31,910 have speeds up to 8kw and almost all will be so-called Type-2 chargers. Unlike chargepoints with a speed of 8kw or faster, chargers below 8kw are not obliged to provide for contactless payment. In fact, the vast majority require drivers to access them via mobile phone apps. What is more, most chargers themselves also need an adequate mobile signal connection to function.

Unless all four mobile operators are providing adequate signal coverage at the chargepoint location there’s a risk that either the user or the charger will lack the connection needed to unlock the flow of electricity, according to RAC Foundation.

Where a 4G signal is absent then a residual 3G signal might still be available, but the national 3G network is due to be shut down completely by 2033. Vodafone has already turned off its 3G network with EE and Three expected to complete their shutdowns later this year, and O2 next year.

Not hassle-free

“Drivers of vehicles fuelled by petrol and diesel are used to reliable and hassle-free filling up at any of the 8,400 forecourts across Britain. The same cannot yet be said of topping up the battery of an electric car at a public chargepoint,” said RAC Foundation director Steve Gooding. “In many instances the mobile phone has become the key to unlocking the potential of the electric car. Unfortunately, that key does not always work.

“The mobile phone is already deeply embedded in our daily lives, not least when it comes to driving where we rely on a good mobile connection to inform our satnavs, pay for parking and to unlock electric chargers,” he said. “But all these systems need to be designed with an eye sharply focused on real-world network coverage, which is often patchy, sometimes non-existent, and not about to become infinitely better.

This study comes as the Society of Motor Manufacturers and Traders (SMMT) reports that the market share of new pure battery electric cars was 15.2% in March compared with 16.2% in the same month last year. The sheer cost of EVs and of EV repairs is already causing palpitations in the motor industry so the mobile issue is only adding fuel to the fire, (or amps).

“Where signal connectivity at a chargepoint is a problem drivers might conclude that the charger is at fault hence undermining the confidence we should be building in the reliability of public charging options for electric vehicles, said Gooding. “What’s more, the poor connectivity won’t get picked up in the new mandatory reporting system applying only to the rapid charger network.”

He added: “In order to design reliable connected services that work for motorists we need a better approach to assessing and reporting the adequacy of on-the-move connectivity so that designers, including electric chargepoint providers, can select which of the readily available workarounds would cover for the shortcomings of the mobile networks.”

Alternatives to patchy mobile

Gooding believes some workarounds could include: signposting the availability of a limited wi-fi hotspot for drivers to use (e.g. in the on-charger instructions for use) if the chargepoint’s connection is robust but the motorist’s might not be; the use of roaming SIM cards (i.e., from other countries); ‘roaming’ RFID cards more widely, and freely, available to remove the motorist’s phone from the equation; or improving the Single Rural Network programme of mast sharing between mobile network operators.

The RAC Foundation analysed a randomly selected sample of 2,059 Type-2 public chargers across Britain. The mobile signal strength data used in the analysis was provided by Teragence.