The Belgium incumbent, Wyre, Telenet and Fiberklaar signed an MoU which should allow them to expand the roll-out of infra in the Dutch-speaking north with less disruption from construction

Proximus and Wyre, with Telenet and Fiberklaar, have agreed to work together on faster, broader fibre deployment with less civic disruption. The intended collaboration would cover about 2.7 million homes across zones with intermediate to low population density.

The parties are yet to reach a final agreement for which they need regulatory and antitrust approvals.

Carving up the territory

In ‘medium-dense’ areas, Wyre and Fiberklaar will deploy FTTH to about 2 million homes if the agreement reaches fruition, of which 60% would be by Wyre and 40% by Fiberklaar. The infrastructure would offer reciprocal wholesale access to this infrastructure for Proximus and Telenet, respectively. This should result in a more efficient roll-out with less disruptive construction works.

In the most sparsely populated zones, Proximus would start offering services using Wyre’s Hybrid Fiber Coax (HFC) network for about 700,000 homes, meaning it could offer gigabit speeds throughout Flanders. In large cities and dense parts of the territory, operators will continue to roll out their own networks separately.

The speed is much needed. Belgium remains a laggard in terms of FTTH/P penetration however. In a blog, ING noted, “Additional investment is particularly required in Belgium, Germany, and Greece,where less than 30% of homes were connected to fibre in 2022 (FTTH Council Europe).

“This stands in stark contrast to Lithuania, Portugal and Romania, which had connected roughly 90% of their households to fibre at the end of 2022. The difference is largely explained by lower costs per premises in South and Eastern Europe, which is why networks overlap more often.”

What led to the MoU?

The signing of the MoU is after months of discussions after the BIPT’s and BCA’s announcements in October 2023 which said they were willing to consider possible collaborations between operators. The parties have identified key terms for a possible collaboration that aligns with the announcements.

The four parties engaging with the BIPT and BCA and will say they will “fully cooperate with the authorities during their investigations”. They also say no further details will be released until the cooperation agreement is formally signed. This is expected to happen in the fourth quarter at the earliest.

Guillaume Boutin CEO of the Proximus Group said, “We have always been open for partnerships that can guarantee a faster and more efficient roll-out of fibre for households and enterprises, making fibre accessible to as many citizens and businesses as possible…

He added, “I am convinced that smart collaboration between operators would ensure optimised deployment and utlisation of the network, which would be beneficial for the consumers, all stakeholders and for the competitiveness of society as a whole.”

Proximus’ Board of Directors has confirmed Guillaume Boutin as Proximus Group’s CEO for a further six years. He became group CEO in December 2019.

The performance in certain segments, particularly VMO2 and Telenet, reveals challenges that need to be addressed, including customer retention and revenue stabilisation

Liberty Global reported a robust consolidated cash balance of $3.5 billion in Q2, bolstered by $420 million from the sale of its stake in All3Media, while delivering strong operational performance in the Netherlands and growing infrastructure investments across Europe. However, these positives were tempered by notable declines in key markets such as VMO2 and Telenet, where revenue shortfalls and customer base declines underscored problems it will need to address. As the telco makes progress with strategic initiatives like the Sunrise spin-off and network sharing agreements, the mixed results showed how much more work needs to be done in the UK and Belgium.

In terms of financials, Liberty Global’s Q2 revenue increased 1.4% YoY on a reported basis and 2.2% on a rebased basis to $1,873.7 million while net earnings (loss) increased 153.8% YoY on a reported basis to $275.2 million. Q2 Adjusted EBITDA increased 0.5% YoY on a reported basis and 1.0% on a rebased basis to $604.7 million. Adjusted EBITDA Growth in Several Segments: Adjusted EBITDA increased in several segments, notably in the Netherlands and at VodafoneZiggo.

Liberty confirmed the spin-off of Swiss telco Sunrise is on track for Q4 2024. That telco’s management team will host a Capital Markets Day in Zurich on 9 September. Sunrise showed strong broadband net additions and an increase in postpaid mobile net adds in Q2, which is encouraging for its future as an independent entity. Meanwhile, Liberty Global made good progress on fibre deployments in the UK, Belgium and Ireland, along with strategic network sharing agreements with Vodafone in the UK and Proximus in Belgium.

However, the telco updated the revenue guidance for VMO2 to reflect a “low to mid-single-digit decline” due to lower handset sales. Telenet also experienced a decrease in revenue driven by a drop in B2B wholesale and mobile revenue. In addition, VMO2’s fixed customer base declined by 13,600, and its postpaid mobile base saw a significant decline of 118,400.

Meanwhile, Telenet’s performance was impacted by a tough comparison to the previous year, with declines in both postpaid mobile and broadband bases. Revenue and Adjusted EBITDA also decreased. Telenet also saw a notable decrease in Adjusted EBITDA, driven by higher staff-related expenses and increased sales and marketing expenses. In the Netherlands, VodafoneZiggo’s broadband base contracted by 22,600, driven by a decline in the consumer segment. Despite the growth in mobile and B2B fixed revenue, the loss in the B2C fixed customer base will be management.

Value over volume

“Against a highly competitive backdrop in the UK our strategy of focusing on value over volume, as well as successful implementation of the price rise, supported a recovery in fixed ARPU,” said Liberty Global CEO Mike Fries. “In Switzerland, we’re continuing to build operating momentum in both the main brand and flanker brands, supporting continued growth in broadband net adds and strong growth in mobile postpaid.”

“We delivered a standout performance in the Netherlands during the quarter, supported by the fixed price rise and solid growth in mobile and B2B,” he said. “In Belgium, as anticipated, a tough comp from the prior year did impact financial performance, but we continue to drive strong fixed ARPU growth, and we’re seeing good trading performance following the launch of our BASE FMC offering nationwide.”

Fries confirmed all 2024 guidance metrics, except VMO2’s revenue. He said this moved from ‘stable to decline’ to ‘low to mid-single-digit decline’. He added that this reflected the continued pressure on low-margin mobile hardware revenues.

Swiss progress

During Q2, Sunrise delivered a second consecutive quarter of broadband growth, achieving 5,000 net adds, primarily driven by reduced churn on the main brand. In mobile, growth in postpaid accelerated, as Sunrise delivered 32,900 postpaid net adds, supported by an improved main brand performance and reduced churn. FMC penetration across the Sunrise broadband base continues to grow steadily, reaching 59% in Q2, an increase of 0.9% YoY. Revenue of $815.8 million in Q2 2024 was flat YoY on a reported basis and increased 0.5% on a rebased basis.

Tough for Telenet

During Q2, Telenet’s postpaid mobile base declined by 500 while its broadband base declined by 4,800. Despite the “intensely competitive market environment”, the sequential improvement was driven by successful marketing campaigns and the launch of BASE Internet and BASE TV in early June. Following the launch of the fixed BASE product in Wallonia and in the Flemish and Brussels footprint, BASE is now a nationwide FMC brand. Earlier today, Telenet announced the signing of a MoU for collaboration on the further deployment of fibre networks in Flanders.

Revenue of $755.1 million in Q2 2024 decreased 1.6% YoY on a reported basis and 0.9% on a rebased basis. The rebased decrease was primarily driven by a decrease in B2B wholesale revenue following the loss of the Voo MVNO contract and a decrease in mobile revenue driven by lower interconnect revenue and handset sales, partially offset by the benefit of the June 2023 price rise.

VMO2 finds it tougher

VMO2’s fixed customer base declined by 13,600 in Q2. Customer growth in the nexfibre footprint continues to build steadily and is expected to rise as marketing increases, however, this was offset by a “moderate loss” on the VMO2 footprint during the quarter when price rises were implemented. Having stabilised in recent quarters, fixed ARPU returned to growth in Q2, growing by 3.1% YoY.

In mobile, the postpaid base declined by 118,400 in Q2. Reflective of wider market trends, activity in the premium end of the market remained lower than the prior year, impacting gross additions, while churn remained stable. VMO2’s full fibre footprint reached the milestone of 5 million premises at the end of Q2. The telco’s fibre build pace increased by 68% YoY, as the total serviceable footprint grew by 295,300 homes in Q2, principally through build on behalf of nexfibre. On the mobile side VMO2 and Vodafone announced a new, long-term network sharing agreement.

Revenue in Q2 2024 was £2,673.7 million, down 0.5% from last year. This drop was mainly because VMO2 sold fewer mobile phones, which affected its overall sales. While they did make more money from their new construction projects and raised prices for home internet services, this wasn’t enough to offset the decline. Additionally, there was a drop in revenue from business-to-business fixed services.

Netherlands solid

During Q2, VodafoneZiggo’s mobile postpaid net adds declined by 18,400, driven by B2B government contract losses. The broadband base contracted by 22,600 in the quarter, as a 27,400 decline in Consumer was only partially offset by a 4,800 increase in B2B. Both mobile and fixed ARPU continued to grow in the quarter, supported by the benefit of the price indexation implemented in October. The FMC broadband household penetration remained stable at 48%. In July, VodafoneZiggo successfully acquired 100MHz spectrum license in the 3.5 GHz band.

Revenue from VodafoneZiggo grew by 0.3% from last year to $1,091.6 million in Q2, mainly due to increased sales from mobile services and business fixed-line services. However, this growth was partly offset by a drop in home fixed-line customers. The telco’s operating profit also improved by 7%, helped by lower energy and consulting costs. Additionally, after accounting for expenses on property and equipment, its adjusted profit rose by 15.5%.

Germany remains a drag on Vodafone while BT shed a record number of broadband customers in a quarter at just under 200,000

Vodafone Group’s profits rose 2.8% in Q1 to the end of June, rising to €9 billion. Africa and Turkey were the stars of the show, while lower inflation was blamed for the lack of growth in Europe.

Total revenue in Africa increased by 3.2% to €1.8 billion due to higher service and equipment revenue. Total revenue increased by 45.6% to €0.7 billion, with service revenue growth somewhat offset by devaluation of the local currency.

Germany, Vodafone’s biggest market continues to drag on revenues. German revenue fell by 1.7% in the quarter to €3.095 billion compared to the same quarter last year. The operator says this “is expected” due to the change in the law that means those living in multi-tenanted dwellings (MTD) are no longer obliged to accept the landlord’s chosen TV service provider but each unit can choose its own supplier.

The change came into effect this July, later than originally scheduled. Vodafone says, “We have continued to migrate end users to new contracts at scale. We continue to expect to retain around 50% of the 8.5 million MDU TV households.”

Focus on the big ticket stuff

The UK, Vodafone’s second biggest country market continues in a state of quasi-limbo (revenues up 0.3% to €1.689 billion while the Competition and Markets Authority ploughs on with its investigation into the possible effects of Vodafone merging with Three UK.

The group’s CEO, MargheritaDella Valle focused on big number income from disposing of assets: “During the last few months, we have announced the final step in reducing our stake in Vantage Towers to 50% for €1.3 billion and commenced our €2 billion share buyback programme following the sale of Spain.

“We continue to progress our transactions in Italy and the UK as well as the broader transformation of Vodafone, focused on customer experience, Business growth and operational execution in Germany. The actions we are taking now will deliver improved performance and underpin the turnaround of Vodafone.”

In line with expectations

Meanwhile, BT Group hasn’t got that much to celebrate either in its first quarter which ended on 30 June. BT reported a 2% drop its underlying Q1 revenue to £5.1 billion. Its EBITDA still rose 1% to £2.1 billion, thanks apparently to “transformation and tight cost control, including lower staff costs,” according to the group’s still new CEO, Allison Kirkby.

She added, “Our ongoing cost transformation contributed to EBITDA growth, and more than offset the expected revenue declines in Consumer and Business in the quarter. There is much more to do to simplify BT Group and deliver for our customers. We remain on track to deliver our financial outlook for this year.”

Putting a shine on it

BT’s semi-detached wholesale fibre unit, Openreach, passed more than 1 million premises in Q1, which is a rate of 78,000 a week. In total, it has now passed 15 million premises and during the quarter, its FTTP customer base passed 5 million. It said, “strong demand for such services has resulted in a 29% year-on-year increase in orders and net additions of 387,000.

On the other hand, it lost a record 196,000 broadband customers in a single quarter as competition and its price hikes bite. Kirby’s positive take on this is that in the Consumer segment, “the widespread availability of FTTP and 5G, combined with our new EE propositions, has contributed to an improved trend in our customer base, in what remains a very competitive market”.

She also highlighted “improved trends” across its struggling Business unit but reported adjusted revenues down 5% from £2 billion to £1.9 billion over the same period last year.

Not helpful

In May Ofcom fined BT £2.8 million after an investigation concluded it had failed to follow clear and simple contract information rules resulting in at least 1.1 million EE and Plusnet customers had not received contract information and key terms before they signed up, such as information on price, speed and early exit fees. BT must also identity and refund any customer who may have been charged an early exit fee on a contract taken out where the correct information wasn’t given.

In addition, earlier this month BT received a fine from Ofcom of £17.5 million for being ill-prepared to respond to a catastrophic failure of its emergency call handling service last summer. BT was unable to connect calls to emergency services between 06:24 and 16:56 on 25 June 2023. During that time nearly 14,000 call attempts – from 12,392 different callers – were unsuccessful.

Local business newspaper Expansión says MasOrange would hold 50% of the new entity, Vodafone 10% and sell the outstanding 40% to investors

According to the local newspaper Expansión, MásOrange and Vodafone are well down the road in talks about creating a joint venture to offer a fibre broadband in Spain. The goal is that the business would be worth €7.5billion to €10 billion.

MásOrange – the biggest converged operator in Spain since the takeover of MasMovil earlier this year by Orange Spain – would own about 50% of the new entity. Vodafone, now owned by Zegona Communications, would hold 10%.

They hope to attract an investor to take the other 40% stake for €1.5 billion to €2 billion. The newspaper pointed out that this would help both of them reduce their considerable debt while maintaining the controlling stake.

The report says the parties expect the negotiations to be concluded by the end of this month.

UPDATE: The Vodafone and MasOrange have confirmed they are forming a fibre JV but they have not confirmed any of the monetary values suggested by the newspaper report.

We dug even deeper than Nokia’s published survey results to find out which sectors look to benefit the most and specifically where return on investment is coming from

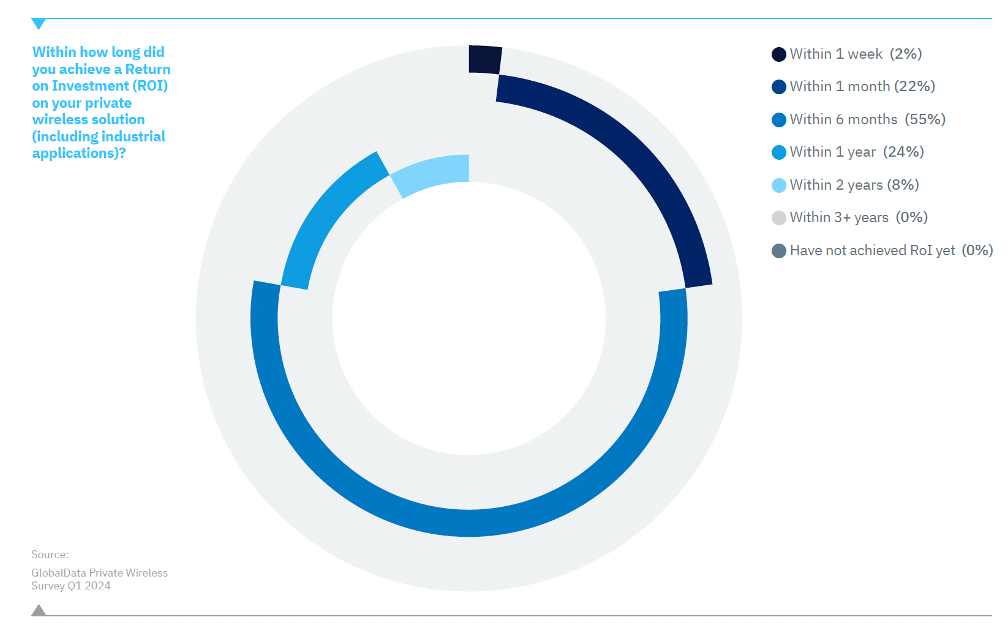

Nokia first partnered GlobalData in 2022 to investigate the private wireless network market. It published Private Wireless Networks Market Opportunity Forecast in December 2022.The stated that 79% of respondents achieved a return on their investment (ROI) in fewer than six months. More than 50% had already seen the total cost of ownership (TCO) fall by 6% or more and 29% had experienced a reduction of more than 10%.

These were interesting findings as the received wisdom at the time was that ROI was perhaps the biggest inhibitor to enterprises adopting private networks.

The report also suggested that the size of the global private mobile market would grown by 49% by the end of 2024, compared to 2022, and almost double by 2027 to be worth close to $8 billion (€7.326 billion) in equipment sales. This is a compound annual growth rate (CAGR) of 23.3%.

Taking a second look

Some 18 months later, Nokia again commissioned GlobalData to undertake research into how the market is progressing. GlobalData conducted surveys and interviews with execs in more than 100 enterprises in industries like manufacturing, transport and logistics, mining, oil and gas, and energy, who have deployed private networks. The companies were headquartered in Australia, France, Japan, UK and US, with 80% operating in two or more countries and 90% have more than 500 employees; about 60% of them have more than 1,000.

Not all the companies interviewed by GlobalData are Nokia’s customers. Some of the qualifying questions were, “Do you deploy a private wireless network? Do you deploy an industrial edge”. Hence the respondents are referred to as “early adopters” that are “scaling and clear about the business benefits”.

One good thing leads to another

One of the most interesting developments identified in the second report is that enterprises are quickly scaling up deployments once they’ve experienced success. Is this music to the ears of telcos who have failed to monetise 5G through enterprise deployments? In our interview, Carlijn Williams, Head of Marketing for Nokia’s Enterprise Solutions business, was quick to point out that neither Nokia’s deployments nor the research are limited to 5G, but also include 4G and Wi-Fi, and that the Gs and Wi-Fi can complement each other.

That said, Williams adds that Nokia is seeing “more and more 5G networks because the device ecosystem is also maturing” in its existing deployments – Nokia now has 760 private network customers, up from 730 at the end of Q1. She adds, “What I also see with our existing customer base is most of them are deploying multiple [private] networks and in multiple locations, and going from one use case to multiple use cases.”

Who makes the decisions?

The proliferation includes more than one location within the same country as well as spreading to other markets. For example, one customer first deployed in Brazil and now is implementing a private network in China. Another deployed in multiple sites initially and for the moment does not appear to be looking at deployments elsewhere.

Also, decisions seem to happen at various layers within organisations. Williams notes, “You have to still convince the local management teams every time”. She added that in Global Data’s research, 20% of the respondents were C-level, 37%, Vice President, Director or Senior Manager level. Then 43% were head of team or department. She adds, “I don’t think you can conclude looking at that that it’s only the top execs who have control over multiple countries, because there’s plenty of heads of department/site facility.

“On the other hand, there’s a lot of VPs and C-level [among respondents] and they are all scaling into multiple use cases and multiple regions. So it helps to have that top management commitment to it.”

Has the RIO profile changed?

Williams says, “I think the big ROI comes from business continuity. Before many of our customers might have experienced connectivity issues with applications…for example, AGVs [automated guided vehicles] AMRs [autonomous mobile robots] and other mission critical applications. Often this was deployed on Wi-Fi and there would be coverage gaps, which means stops and starts for the AGVs, etc. If that no longer happens, you see the ROI. I think that’s the main reason why this is happening so fast.” See graph below.

Of those customers that started with AGVs or AMRs, Williams says there is a cycle time increase of roughly 25% compared to Wi-Fi, “so that’s an immediate impact on productivity. Many of these customers are now expanding around them, adding licence plate recognition, or alarm buttons for our workers because they have that mission critical connectivity and often the edge too to deploy these [real-time] use cases,” she adds.

Edge is the beating heart

Williams continues, “the edge is very critical for us”. This is because in private networks, every deployment is different in terms of the location, the applications, the systems, the organisations’ activities and objectives, and so on. It’s not simply a case of replicating the same thing over and over, yet scale is essential in terms of speed, cost and simplicity.

“That’s why we lead with the edge,” Williams explains. “That’s why we deploy or pitch Nokia One Digital Platform because it is simpler and faster to deploy. It starts with the mission-critical in industry and digital edge is the beating heart of it. Of course, you can have private wireless deployed on it and Wi-Fi and they can work together, but edge is the beating heart and you can scale out from that.”

She adds, “First we work with partners to set up the network and make sure it can penetrate everywhere – no coverages holes and small cells in exactly the right places. Once it is deployed, as we found in the survey and some in-depth interviews, many customers say it is as easy to maintain as a Wi-Fi network.”

The second survey reveals that at the moment, about 39% of those early adopters have deployed an edge, with a further 52% planning to do so. She states this proves that, “The vast majority see the value of the edge because if the data is kept on-prem with low latency, industrial customers can deploy things like high definition video for quality control, for example.” See section on use cases below.

Which sectors enjoy the best ROI?

Did the survey give any indication of which sectors are gaining the greatest return on investment? Williams says the early adopters interviewed largely came from manufacturing – 44% discrete (that is the making of distinct items) and 31% process manufacturing (creating goods by combining supplies, ingredients or raw materials using a predetermined formula), petrochemical oil and gas. Transportation, ports, airports, warehouses and logistics made up 10% and a further 10% was energy.

Discrete

Process

Within 1 week

2%

3%

Within 1 month

20%

19%

Within 6 months

52%

61%

Within 1 year

11%

13%

Within 2 years

14%

3%

Source: Global Data/Nokia

So 83% of process manufacturers (26 out of 31) expect to achieve an ROI within six months, compared to 74% of discreet manufacturers (33 out of 44) over the same period.

Increase in Productivity:

Process

Discrete

Rank 1

23%

20%

Rank 2

10%

25%

Rank 3

19%

2%

Rank 4

6%

7%

Rank 5

0%

0%

Overall

58%

55%

Source: Global Data/Nokia

Overall 58% of process manufacturers (18 out of 31) rank productivity as one of their top five benefits, compared to 55% of discreet manufacturers (24 out of 44). When analysing the top two benefits, the gap is more significant – 45% of discreet manufacturers (20 out of 44) select this as one of their top two benefits compared to 33% of process manufacturers (10 out of 31).

Identifying the ‘right’ use cases

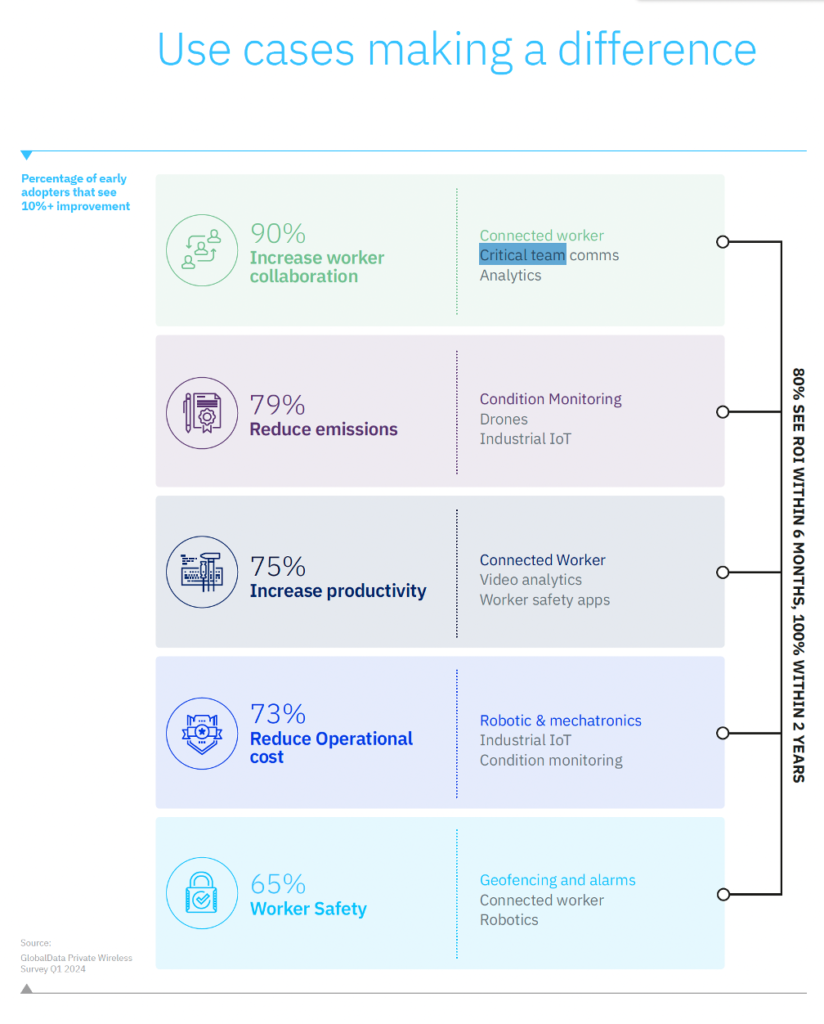

Williams says, “Another difference with the research the second time among the 100 early adopters is to break that down those business benefits and quantify them with numbers. We asked, “What do you see in terms of improvement in terms of all these work, collaboration, reduce reduction of emissions, productivity increases, etc?’.”

She says the most surprising was that work collaboration scored the most highly (see infographic below), with 90% of respondents said they have seen an improvement in work collaboration, ranging from 10% to 30%. The use case most commonly responsible for this increase was connected worker, the second was ‘critical team’ and the third analytics.

Three biggest reasons to invest in digitalisation

Another major finding, in Williams’ view, is three biggest drivers for investment in digitalisation. Number one is productivity. Number two is workers’ safety. Number three is sustainability – so the reduction of emissions and energy [consumption] to reach these ECG [economy for the common good] targets.

She says, “Let me start with emission reduction – 79% of the early adopters saw a reduction of over 10% in their remissions [as regulation bites, this is going to become ever more important]. The number one use case is condition monitoring, number two is drones, such as for inspections of difficult and dangerous to reach places, and number three is industrial IoT.”

Then 65% of the 100 early adopters saw an improvement of 10% in safety in the workplace, including a reduction in the number of accidents. Geofencing where alarms was the most deployed use case, but also connected worker and robotics to replace people in some of the dirty or dangerous work because they have a private wireless network and industrial edge deployed.

She says there are many kinds of connected worker use cases: “For example, big chemical and petrochemical plants want to go paperless so they’re giving all their workers handhelds and devices to provide data at their fingertips rather than on a clipboard. Workers no longer have to walk from one place to the next, often across huge plants, or drive. They have their devices to communicate with each other and access data. They have applications for remote maintenance, etc.”

And one thing tends to lead to another with connected worker. The report describes one instance one manufacturing business’ original use case was to connect hand scanners in the warehouse. This expanded to include automation and maintenance solutions, including employees wearing connected Google Glass devices so machine manufacturers to diagnose faults remotely. This means their engineers turned up knowing what they needed to fix and properly equipped for this job.

Let’s hope report number three focuses on new revenue streams.

Partner content: Alongside its many social and economic benefits, the internet also provides a massive venue for people to commit or be victimized by, online crime

From financial fraud to stalking, many of these transgressions are much older than the technology used to perpetrate them, but digitization helps criminals offend more efficiently, as with scam emails or recruiting ad hoc groups of people to attack others online.

The rapid growth of AI adds to that reality, fueling both the crimes themselves and the law-enforcement response to them. Generative AI, with its ability to spontaneously create realistic language, photos, and video, takes this trend to a dangerous new level. As is often the case, the most vulnerable in society – particularly children – suffer a disturbingly large share of the harm and recently the FBI put out a warning specifically regarding this threat.

Grooming children – a systematic violation of trust

Online crimes against children often begin with the perpetrator deceiving victims to build rapport and gain their trust, posing as another child with shared interests, for example. This “grooming” often convinces the victimized child to post indecent photos or videos of themselves that are eventually traded or sold online. That distribution may occur on the dark web or be thinly disguised beneath the surface of legitimate venues such as social media.

Regrettably, technologies and techniques created for legitimate marketing functions can be adapted for this purpose. For example, AI chatbots can carry on lifelike conversations with potential victims, and those tools are becoming increasingly sophisticated. Intended for usages such as automated cold-calling or customer support, this software can provide realistic, compelling written conversation and even speak directly to victims using a range of selectable voices and personalities.

Automating this part of the grooming process makes criminals much more dangerous by increasing the scale of their reach. Traditionally, these bad actors were limited by the need to interact directly with the children they targeted, which might require many conversations and substantial effort. AI and related technologies can reduce that effort significantly, from machine learning that identifies potential grooming victims based on their online presence to generative AI bots that carry on illicit conversations with them.

Terrible new frontier – “Deepfake” CSAM

A new generation of computer-generated child sexual abuse materials (CSAM) can be created by generative AI. These pictures and media could potentially be an even greater threat to society than “authentic” materials because they can be generated at massive scale and limited only by perverse imaginations. Deepfake CSAM does not require grooming and is created using legitimate images from social media or other lawful online venues – an extremely common practice.

Deepfake CSAM campaigns that feature celebrities and other publicly recognizable personalities –which would likely be impossible to generate otherwise – could be especially desirable and/or lucrative for criminals as well. The potential for such materials to receive increased public attention could make them more traumatic to victims.

Whether deepfake CSAM depicts real people or not, it has the potential to extend the toll these crimes take on individuals and society. Moreover, it reduces the need for violators to interact with their victims, making their actions more difficult to detect. Rather than spending months establishing contact with and manipulating a victim, perpetrators can act rapidly and independently. This leaves fewer clues and less potential for detection by law enforcement and others committed to protecting children.

Complexity and hope of mustering a response

As is too often the case, law enforcement agencies (LEAs) find themselves in a struggle with criminals for technological dominance. Identifying potential violators (as well as their potential victims) is challenging because of the technological scope and complexity and building a case to stop the harm and prosecute the perpetrators is even more difficult. As these crimes evolve by means of AI and more, LEAs must rise to the challenge with similar technologies and corresponding tactics.

For example, an LEA could create a decoy site that appears to be run by a child or pose as a potential grooming victim. These measures are well-suited to the use of AI to increase reach, but the skills required to execute such an operation are in short supply within the LEA community, just as elsewhere. Budgetary considerations add to the difficulty. Usability of these tools will increase, but in a head-to-head escalation of skills and tactics, criminals may sometimes have the upper hand.

In response, the struggle to prevent AI-assisted crimes against children will continue on many fronts, including by dozens of not-for-profit organizations. For example, the Internet Watch Foundation (IWF) has developed mechanisms to digitally and automatically identify CSAM using MD5 hashing. SS8 draws on this work, incorporating the IWF CSAM hash list in its next-generation Intellego XT lawful monitoring center to help LEAs counter the potential harm to children, the investigators who must review CSAM material, and society at large.

About the author

Kevin McTiernan has over 20 years’ extensive experience in the telecommunications and network security industries. At SS8, Kevin is the VP of Government Solutions and is responsible for leading the vision, design, and delivery of SS8’s government solutions, including the Xcipio® compliance portfolio. You can learn more about Kevin on his LinkedIn profile by clicking here.

About SS8 Networks

As a leader in Lawful and Location Intelligence, SS8 helps make societies safer. Our commitment is to extract, analyze, and visualize the critical intelligence that gives law enforcement, intelligence agencies, and emergency services the real-time insights that help save lives. Our high performance, flexible, and future-proof solutions also enable mobile network operators to achieve regulatory compliance with minimum disruption, time, and cost. SS8 is trusted by the largest government agencies, communications providers, and systems integrators globally.

Intellego® XT monitoring and data analytics portfolio is optimized for Law Enforcement Agencies to capture, analyze, and visualize complex data sets for real-time investigative intelligence.

LocationWise delivers the highest audited network location accuracy worldwide, providing active and passive location intelligence for emergency services, law enforcement, and mobile network operators.

Xcipio® mediation platform meets the demands of lawful intercept in any network type and provides the ability to transcode (convert) between lawful intercept handover versions and standard families.