The former ETNO says that for the first time in seven years, total telecom investment in Europe has declined by 2%, from €59.1bn in 2022 to €57.9bn in 2023

Connect Europe (CE) has published its annual review of telecoms and digital in Europe, estimates for the first time the worth of Europe’s connectivity ecosystem. While the association has an agenda which adds a pinch of salt to the numbers it produces, the overall trends are sobering for the industry.

Europe’s telecom sector faces mounting financial and structural challenges, jeopardising its ability to stay competitive on the global stage. In 2023, European telecom revenue declined by 4.4% in real terms as operators struggled with rising inflation. In 2023, mobile ARPU in Europe remains the lowest globally at €14.8, starkly contrasting with €41.7 in the USA, €26 in South Korea, and €22.6 in Japan.

Regardless of the right and wrongs of “fair share” arguments – which always seem to ignore the market distortions caused by monopolies in adjacent markets like search and cloud – CE is right to point out the lack of market consolidation in Europe hinders growth, limits economies of scale, and stifles competitiveness, creating additional obstacles for the sector. In 2024, Europe had 41 large mobile operators (over 500 000 subscribers), compared to just 5 in the USA, 4 in both China and Japan, and only 3 in South Korea.

“Strong and innovative operators are crucial to build a European technology stack and boost competitiveness. Deregulation and more scale are both needed to free up investment and ignite innovation,” said Connect Europe director general Alessandro Gropelli.

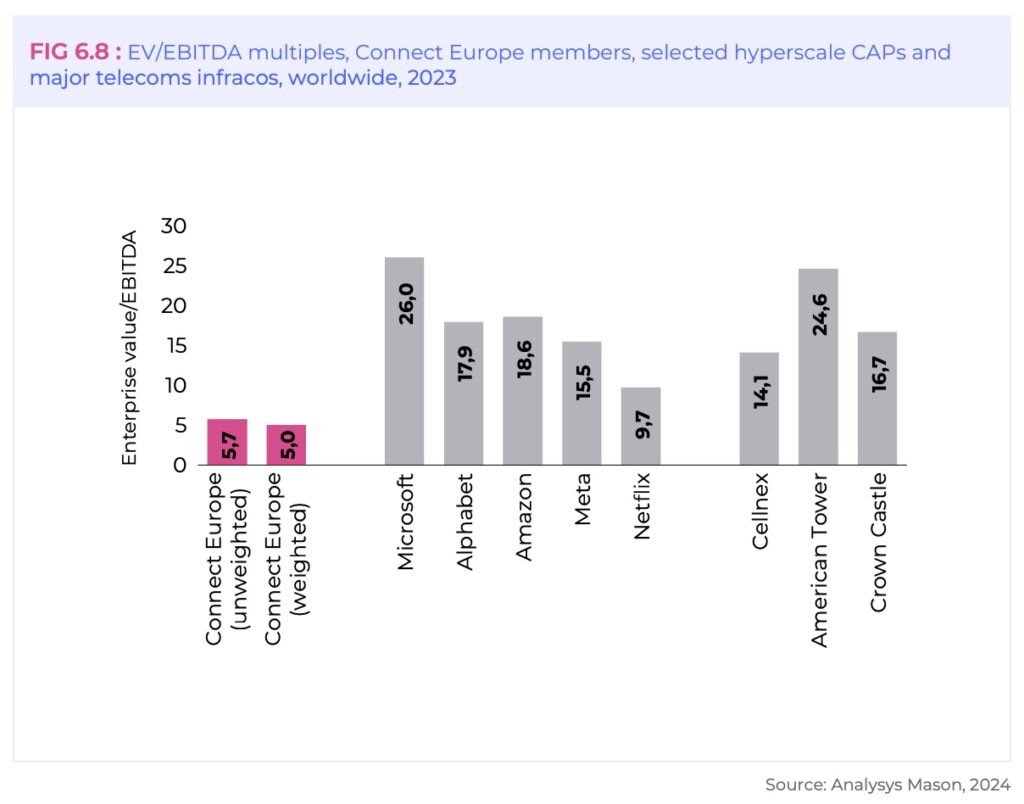

Connect Europe said its findings confirmed the European telecoms market is “excessively fragmented and over-regulated”.

Report card

The report tracks progress on network innovation and shows Europe as still being weak on critical technologies such as 5G SA and edge cloud, but making inroads – gradually – on Open RAN, network APIs, AI for network operations and R&D for 6G. Overall, it is a mixed bag of results with even the good points containing a sting in the tail. Although Europe has made progress in critical areas, it still lags behind global peers. For example, 5G Standalone (5G SA) reached only 40% population coverage in Europe by the end of 2024, compared to 91% in North America and 45% in Asia-Pacific.

CE said Europe’s FTTH coverage of the population reached 70.5%, outperforming the USA (54.8%). Despite this progress, estimates indicate that approximately 45.4 million Europeans will still lack access to a fixed gigabit connection in 2030, falling short of the EU Digital Decade targets.

Alarmingly for the operators, said CE, for the first time in over a decade, total telecom operator investment in Europe declined by 2% in 2023, dropping from €59.1 billion in 2022 to €57.9 billion. This downward trend happens at a time when Europe is still far from its gigabit targets. In addition, investment per capita also lags significantly, with Europe at €117.9 compared to €187.6 in Japan and €226.4 in the USA.

Revenues and investment remain interlinked. The report finds that European operators have effectively absorbed inflation on behalf of their customers, meaning that revenue decreased in real terms. In 2023, European telecom revenue declined by 4.4% in real terms, as opposed to the Consumer Price Index, which increased by 6.4%.

This is a big deal, regardless of where you site in the debate, given the connectivity ecosystem – comprising telecom services, network equipment, and content & applications in Europe – “was worth about €1 trillion in 2023, contributing 4.7% of the continent’s GDP and surpassing traditional industries like agriculture, fisheries, and forestry combined.” However this figure includes equipment vendors, content and application providers, software, the film, TV and music industry and data centre providers so the actual telecom number must be lower.

This ecosystem, said CE, directly and indirectly employs over one million individuals, with Connect Europe members providing essential services to 276 million Europeans alone.

The total investment in the market (including tangible fixed assets and R&D) amounted to €115.5bn, with telecom operators in the lead, representing 60% of the total, followed by content and application providers (just over 30%) and equipment manufacturers (almost 10%).

Bang for the buck

Competition expert Richard Feasey delved into the numbers in the report and came to the conclusion that while Europeans are getting less in absolute terms than their American counterparts, what they are getting might represent better value for money – when adjusted for GDP/capita.

“European consumers spend only 37% (per capita) of what Americans spend on telecoms and their operators receive only 60% of the mobile ARPU and 68% of the fixed ARPU which American operators receive,” he posted in LinkedIn. “Nonetheless, European telecom operators spend 88% (capex per capita) of what American operators spend.”

“And in return, European consumers get 127% of the FTTH coverage Americans get, 91% of the gigabit coverage and 88% of the 5G coverage that is available in the US,” he added.

Connect Europe sees this differently suggested that the discrepancy between telecom services spend as a proportion of GDP in Europe and in the other advanced economies shows that regulatory initiatives have “likely resulted in artificially low prices, arguably below consumer valuations”.

The organisation argues that low prices may be good for consumers and businesses in the short term, but they are not fit for encouraging long-term investment in innovative services, network evolutions or for investing in network coverage where the commercial case is marginal: “indeed they often make the commercial case for network expansion non-existent”. Revenue per used gigabyte of mobile data in the USA is 159% higher than in Europe.

While this argument will be viewed poorly by regulators, allowing more M&A in the sector would improve many of the numbers at least and not necessarily just revenue and economies of scale will also come into play.

The report concludes be stating that the Budapest declaration in November 2024 was a call to action to realign European industrial policy to make Europe more competitive especially in the tech sector that will drive most new growth. CE believes there is now real political impetus, and an opportunity for change “that should not be squandered”.

The communications sector has suffered from many of the problems faced by other sectors, but Connect Europe reckons it is also a key industry to scale up tech growth and green transition. For the communications sector the successful implementation of a pro-growth industrial policy that would meet the challenges Europe faces “requires a rethink of the long-standing competition policy in the sector”.

Several commentators have slammed the report as containing several contradictions, although most recognise there is a sectorial problem that needs fixing. Most, except perhaps Connect Europe’s nemesis Computer & Communications Industry Association (CCIA Europe). That organisations’s SVP and head of office Daniel Friedlaender posted on LinkedIn: “The ‘report’ is basically repackaged whinging from 2013 to justify bleak and drastic changes that won’t do Europe any good and would only precipitate businesses and users moving away from the old school telecom companies to better, more cost effective and innovative alternatives.”

{kind=link}